Businesses accepting payments via cards may face a situation where a chargeback request is raised for a refund to the customer.

What is a chargeback?

A chargeback is a request raised for return of funds to a consumer, initiated by the consumer’s card issuing bank.

It is a form of consumer protection from fraudulent activity committed by both merchants and individuals.

It is best to avoid any kind of chargeback, as banks and card networks can label your business as a high-risk business. A high number of chargebacks could lead to the banks holding remittances for the business and they might also ban the business’s online payment services.

What are the key parties involved in a chargeback?

- Cardholder: The owner of the card involved in the transaction.

- Merchant: The party who sold the goods or services being disputed.

- Issuer: The bank who issued the card to the cardholder.

- Acquirer: The bank tasked with acquiring payment on the merchant’s behalf.

- Card Association/scheme: The card brands (Visa, Mastercard, etc.) who oversee the process.

- Payment Gateway: The payment gateway used to pay money.

What can be the reasons for a chargeback request?

A chargeback request may be raised for various reasons, such as:

- Service or product not received

- The product doesn’t match the description, damaged product, etc.

How does the chargeback process work?

- The cardholder (Ms. X) disputes a transaction by contacting the card issuer (SBI). The issuer (SBI) then gets in touch with acquirer (HDFC Bank) through the same network, the transaction took place, the acquirer (HDFC Bank) then gets in touch with the payment gateway (Cashfree) and payment gateway (Cashfree) will contact the merchant (merchant.com) asking for details depending upon the line of business of the merchant.

- The turnaround time will be provided to the merchant (merchant.com), and in the case of a chargeback, the responsibility lies with the issuer bank (SBI).

- After submitting proof, banks can take up to 21 to 45 for a conclusion, typically called the representation time.

- The chargeback process ends if merchant doesn’t provide the necessary response, after which the cardholder would be reimbursed.

- The time limit to raise a chargeback for the end-user is 90-120 days.

- In case of a chargeback, the same amount will be blocked from merchant.com’s unsettled amount and will be released or refunded on the basis of the result.

Here’s what happens in both scenarios:

- The merchant (merchant.com) decides to respond: the merchant will have to provide evidence related to the order and the transaction. It could be an email conversation, invoice, etc. The proof is passed to the issuer (SBI).

- If the issuer (SBI) accepts the proof/evidence, the chargeback request will be declined. However, the customer would still have the option to chargeback the transaction again, which is called Second Presentment, Second Chargeback (Mastercard), or Pre-Arbitration (Visa).

- If the issuer (SBI) rejects the proof/evidence then the chargeback will be held valid and funds will be reversed to the consumer’s card/account

- The merchant (merchant.com) decides not to respond: The chargeback will be ruled in favour of the card holder and the money will be reversed to his/her account/card.

What happens when a cardholder raises a Second Presentment, Second Chargeback (Mastercard), or Pre-Arbitration (Visa)?

If the first chargeback request is raised by the cardholder but the merchant (merchant.com) wins the claim, the customer would still have the option to chargeback the transaction again and called as Second Presentment, Second Chargeback(master card), or Pre-Arbitration(Visa).

In this case, the merchant is still required to respond with all possible evidence and arguments.

If the merchant decides not to respond: The chargeback will be ruled in favour of the card holder and the money will be reversed to his/her account/card.

If a merchant is to dispute the chargeback, what documents need to be furnished?

The merchant needs to aggregate compelling evidence related to the chargeback. Their evidence can spread across various data sources and may vary depending upon the line of business.

Pro Tip: We suggest that merchants keep these documents ready from day one, so in case any chargeback arises, you will be ready to tackle it.

In general, merchants are required to furnish the following documents:

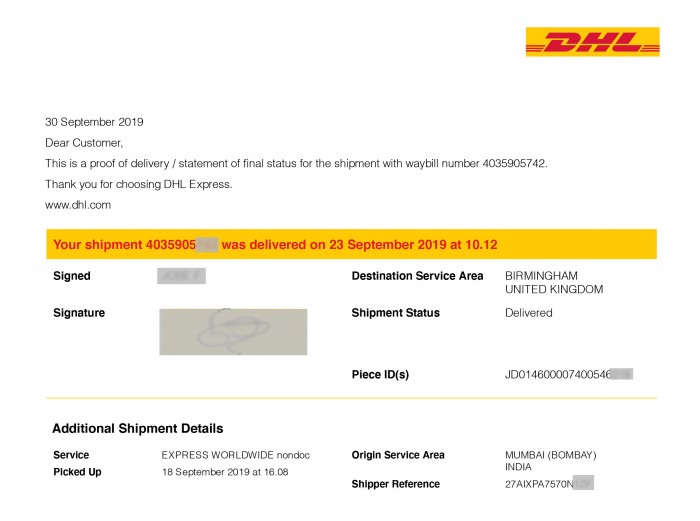

Proof of delivery: Usually in the form of a tracking number, shipping receipt, etc.

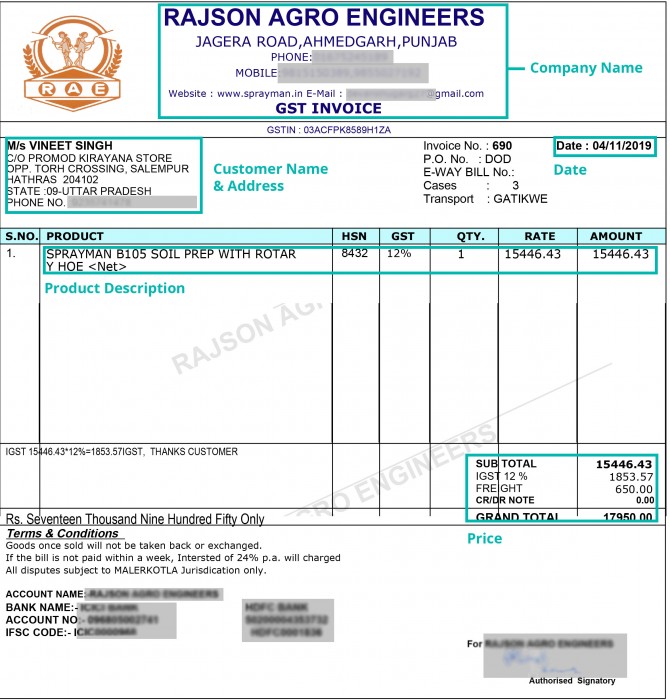

Invoice copy: This should include your company name, price, and description of the product, date, customer’s name and address, date.

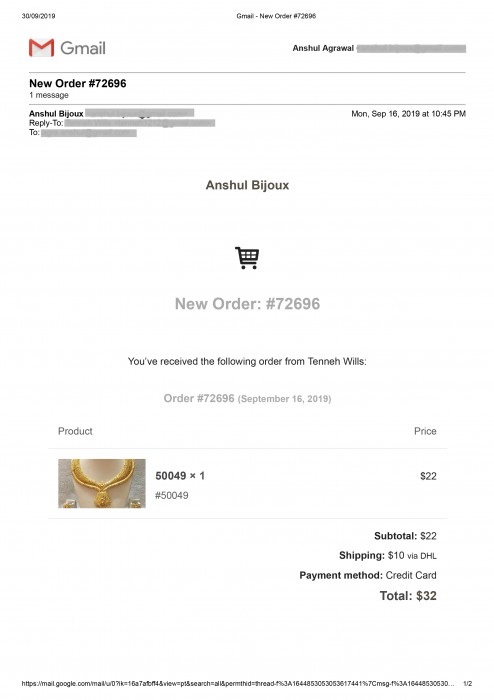

Order confirmation email: This email provides customers with post-purchase reassurance. It should mandatorily include confirmation of your customer’s request (booking, registration, subscription and order) and the order summary.

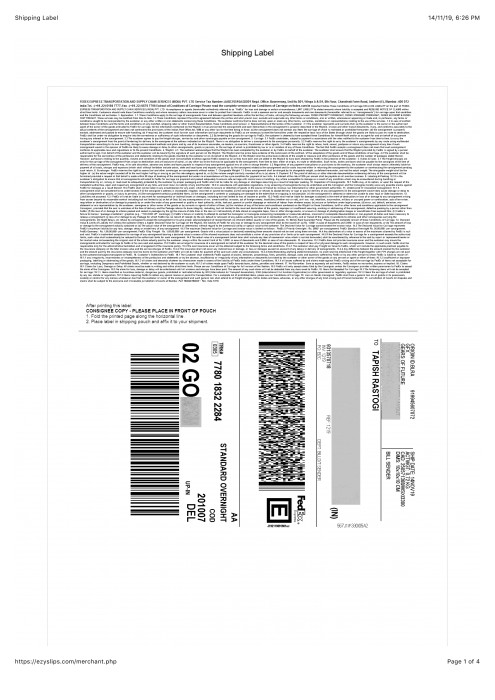

Tracking details: Shipment tracking details provided by the courier delivery company (Not applicable for all).

Finally, we are near the end of the chargeback process. The issuer now reviews the chargeback claim and the merchant's evidence. Each card network requires specific information to prove or disprove a dispute. The required information is typically listed in the network’s rules and regulations.

What are the various stages of chargeback and their respective lifespan?

Let’s say the merchant wins a chargeback. The cardholder could still dispute the outcome. This takes on various names depending on the card network. For example, Visa calls this Pre-Arbitration while Mastercard calls it a Second Chargeback. However, the process is basically the same as mentioned below:

Level 1/Phase 1: Chargeback

Level 2/Phase 2: Second Presentment, Second Chargeback, or Pre-Arbitration: This gives the acquirer and the issuer a second chance to resolve the customer’s dispute. An issuer may issue pre-arbitration for several reasons. Some include:

- A reason code change

- The cardholder offers new information

- The issuer believes the acquirer’s evidence does not disprove the dispute

- Terms and Conditions, or maybe Return Policies that weren’t properly disclosed during the transaction

Level 3/Phase 3: Arbitration: There are explicit time limits that issuers and acquirers must meet in order to file for, and respond to, an arbitration chargeback. There are also implicit time limits for merchants to take action. For example, Mastercard gives issuers and acquirers 45 days to file this action. But they need to have submitted their documents well before in order to thoroughly review and submit it via Mastercard. You can follow the link provided to check the rates associated with the arbitration (https://chargebacks911.com/arbitration-chargeback/).

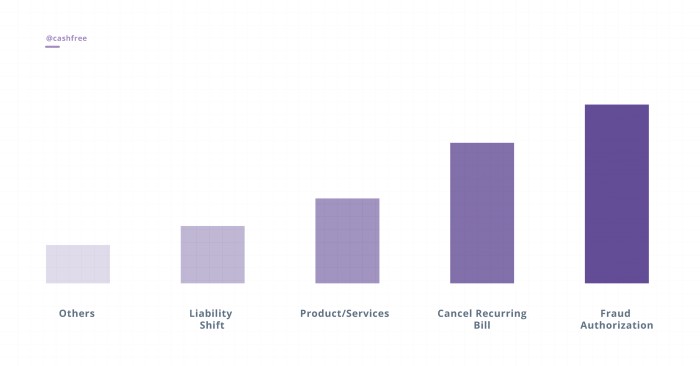

What are the different types of chargeback requests?

There are 151 reason codes to categorize chargebacks across Visa, Mastercard, and American Express.

Reason codes can be categorized into five main categories: Fraud/No Authorization, Cancel Recurring Billing, Products/Services, Liability Shift, and Others.

Overall, Fraud/No Authorization chargebacks account for the maximum number of all disputes. Cancel Recurring Billing disputes represent the second largest percentage of chargebacks. Product/Service chargebacks are a close third. Liability Shift and Other chargebacks represent a small percentage. You can refer to the link provided for more information: (https://chargeback.com/5-chargeback-reason-code-categories/)

As a business, how can I avoid chargebacks?

- Generally, cardholders have an advantage over merchants as credit card companies and banks understand that ultimately, it involves cardholder’s money.

- No matter where you are in the chargeback process, you’ll need to have proof/evidence ready if you want to challenge the dispute. We suggest saving the proof in an easily accessible location, like a folder on your desktop or on your Google drive.

- Be attentive when disputes and chargebacks arise and quickly respond when retrieval requests come in. If you don’t respond within the stipulated time frame, banks automatically process the chargeback. Be ready with an action plan on how to handle chargebacks.

Questions?

We're always happy to help with any questions you might have. Search our documentation, contact support, or connect with our sales team. You can also chat with our team via chat for real-time support.